Buy the Home, Rent the Rate

What Happened to Mortgage Rates?

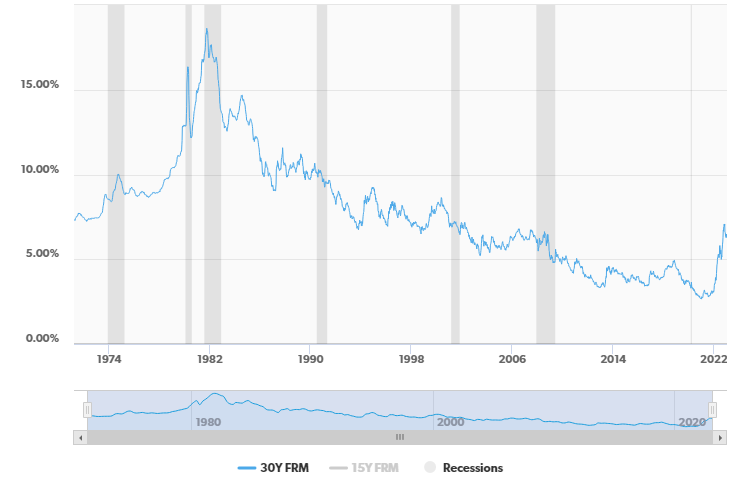

In early January 2021, mortgage interest rates were at all-time historical lows. Per Freddie Mac’s Primary Mortgage Market Survey, the U.S. weekly average at that time was 2.65% for a 30-year mortgage. Flip the calendar forward to mid-November 2022 and the same 30-year mortgage averaged 7.08%. In less than two years, the mortgage interest rates increased by almost 270%, which was the sharpest increase as a percent since Freddie Mac has been tracking rates. The only time the actual rates increased at a more rapid rate was in the early 1980s when a 30-year mortgage went from 12.20% in August 1980 to 18.02% in November 1981. From 1981 to January 2021 there was a slow and steady decline in mortgage interest rates.

Buy the Home but Rent the Mortgage Rate!

Where will rates be in the future? That is the big unknown. Statistically speaking, if you flatten out the above rate curve with the early 1980s as an anomaly of very high rates and the 2010s anomaly of very low rates, the rates tend to trade in the 5.00% – 7.00% range. An immediate response is that mortgage rates are currently too high. That is true when you look at the history from the end of the recession in the late 2000s, but historically that may not be the case – sub-5.00% rates don’t come around too often.

There is an old saying in the mortgage industry that you “buy the home but you rent the rate.” I tell my customers that if they find a home that they love and can afford the payment, they should purchase the property. Don’t worry if interest rates are too high because at some point, the interest rates may come down and they may be able to refinance, but that same home may not be available to be purchased when interest rates are lower.

What Mortgage Product is Right for Me?

What mortgage product should you choose? Most homeowners pick a mortgage that is amortized over 30 years to try to keep their monthly payments as low as possible. However, a 30-year mortgage does not have to be a fixed interest rate. Over the last 15 years, fixed-rate mortgages have been exceedingly low but now that we have headed to a point of higher interest rates, an Adjustable-Rate Mortgage (ARM) may be a product to consider.

If you are considering an Adjustable-Rate Mortgage, make sure that you understand the terms of the mortgage and not just the initial rate. In today’s market, it may be wise to consider an ARM with an initial interest rate locked for an extended period (5-7 years). Look into how often the interest rate changes over the life of the loan as some ARMs will adjust every six months to follow the fluctuation of the market. Ask your lender about the index, margin, and caps. These three items affect how the interest may move over time.

At Stillman Bank, we offer a unique ARM product called a “6/36 ARM.” The initial interest rate is fixed for 6 years and can adjust every 36 months thereafter to help prevent rapid and repeating payment shock. However, depending on your circumstances, our ARM product may not be the best option for you. Some people may just sleep better knowing that a fixed rate loan is locked in for 30 years but have the peace of mind knowing that they are just “renting” that rate and can consider a refinance in the future. Our lenders are here to discuss the advantages and disadvantages of each of our mortgage products so that you can select the loan that is right for you and your family.

Also, don’t forget about the other costs of owning a home, such as homeowners’ insurance and property taxes. Our mortgage lenders review all the costs with you to make sure that it’s a payment that comfortably fits your budget. We have experienced mortgage lenders available at all of our six offices to assist you with the purchase of your new home.

Patrick J. O’Gorman

Senior Vice President

NMLS No. 468516

Opinions expressed are solely my own and do not express the views or opinions of Stillman Bank.