Understanding Credit Scores and Their Impact on Mortgage Lending

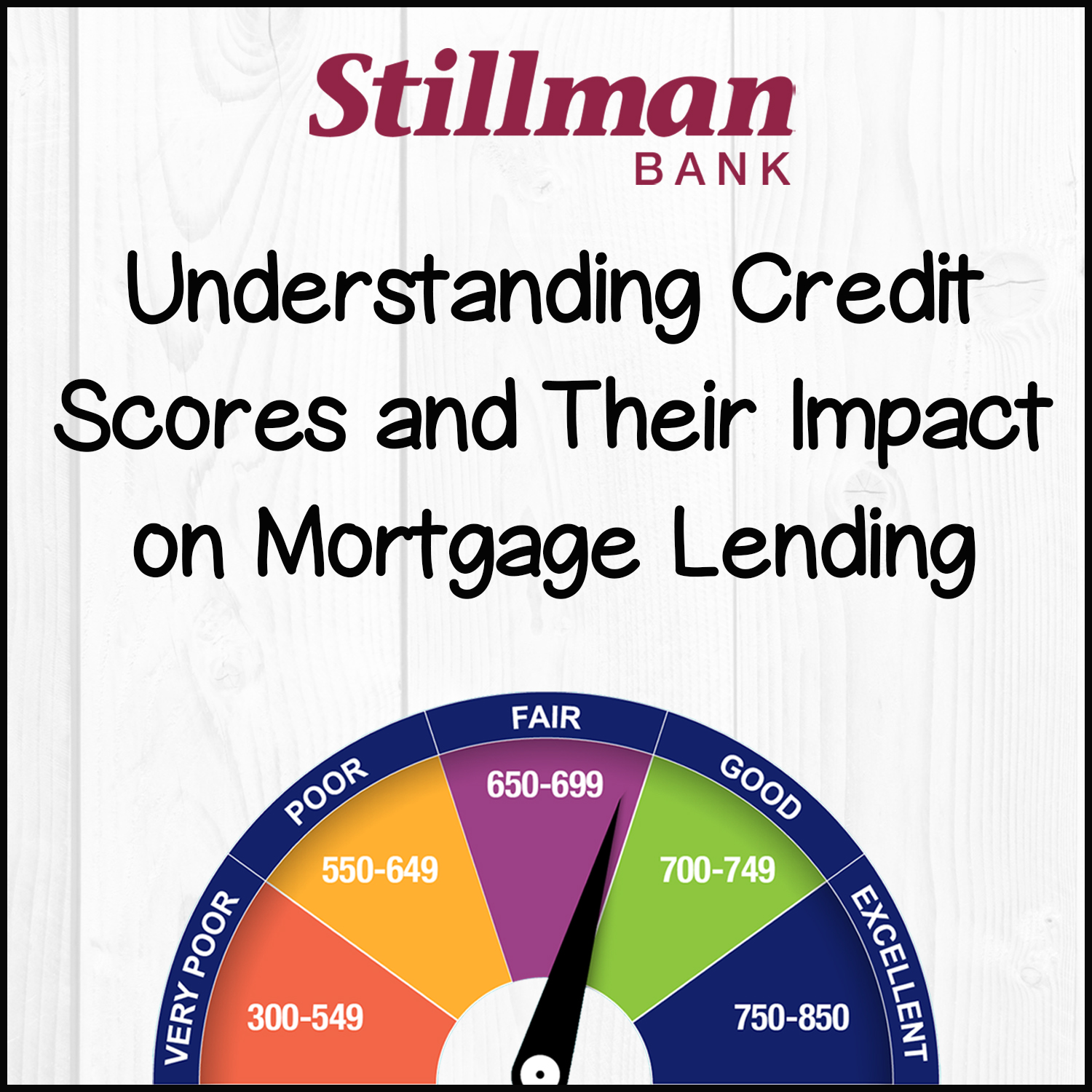

When it comes to applying for a mortgage, your credit score will play a critical role in determining your eligibility. In its most basic terms, a credit score estimates how likely you are to pay back the money. A three-digit number, typically between 300 and 850, is assigned to you to represent your credit risk.

How are credit scores calculated?

Credit scores are calculated using the information found within your credit reports. Certain aspects of your credit report are weighed on a higher scale than others. Below is a percentage breakdown of how a typical credit score is determined.

35% of credit score = Payment History

30% of credit score = Balance vs. Credit Limit

15% of credit score = Types of Credit (credit cards, student loans, mortgages, etc.)

10% of credit score = New Credit/Credit Inquiries

10% of credit score = Length of Credit History

Why it is important to have good credit?

Now that we have established how scores are determined, why is it is so important to maintain a higher credit score? Since many businesses look at your credit score to determine credit risk, individuals with a higher score generally receive more favorable credit terms. This can translate into lower payments and lower interest rates over the life of a loan. An individual with a higher credit score is also able to obtain insurance at a lower rate and establish utility services in their name.

Most lenders will need to have 3 tradelines in your own name reporting on your credit report for at least 12 months to help determine if you qualify for a mortgage. To make sure your credit score is up to par with mortgage requirements, check your credit on your own first. Federal law allows you to get a free copy of your credit report every 12 months from each of the 3 credit reporting agencies (Equifax®, ExperianTM, and TransUnion®). To request your free report, go to www.annualcreditreport.com

What are some common credit problems & possible solutions?

Limited or no credit history

If you have no credit history, ask a trusted family member or friend to co-sign on a loan or credit card for you in order for you to begin building up credit. It is important to note that if you are unable to make payments, the co-signer will be held responsible for paying. In order to protect your co-signers credit score and grow yours, be sure to pay off the entire balance of the loan or card each month. Another possible solution is to apply for a secured credit card – a credit card that requires you to put a deposit down as collateral for opening the card. A secured card is a way to establish a credit history which, if paid off regularly, can help you become eligible for unsecured cards in the future (ones that do not require collateral to open).

A pattern of late payments on current debts

Life happens and an emergency can cause one to miss one or two payments on current debts. It becomes an issue if late payments become a standard occurrence. It is also worth noting that the length of a late payment does affect how much your credit score will decline. For example, a 90-day late payment is much more damaging to your score than a 30-day late payment. In order to combat this problem, pay off all late payments as soon as you are able while continuing to pay the current amount due. However, do not expect immediate results when it comes to raising your credit score. A late payment can often affect your credit report for upwards of seven years.

Charge-offs

If you miss too many payments, a creditor can choose to list your account as a charge-off and stop you from attempting to make additional charges. Regardless of debt type, a charge-off is often the last resort, as this is taken on as a loss for a credit company. Even if your account has been charged off, you are still responsible for paying back the debt. While you may be able to negotiate payment with your original lender or work with a collections agency on paying off this debt, a charge-off can remain in your credit history for up to seven years.

Other common credit problems include foreclosures or repossessions, poor credit performance, bankruptcies, and judgments or liens. In order to circumvent these problems from occurring from the very beginning, it is important to do the following:

- Make monthly payments on time

- Do not use more than 30% of the available credit on revolving accounts

- Do not open a lot of new credit at once (multiple new accounts can adversely affect the score)

What else do mortgage lenders consider?

While your credit score is a key component in determining whether you qualify for a mortgage, it is not the only factor that mortgage lenders consider. Lenders also consider income, employment history, debt-to-income ratio, how much of a down payment you are able to afford, and amount of funds you have available in your savings.

Diana D. Davidson

Mortgage Lender

NMLS No. 746408

If you have additional questions or concerns about your credit score, our mortgage lenders would be happy to review your reports and advise you along the path to homeownership.

Opinions expressed are solely my own and do not express the views or opinions of Stillman Bank.